Most insurance organizations already know their legacy systems are a problem. What they underestimate is how quickly the cost of inaction is compounding. In 2026, the gap between carriers running modern insurance software and those still managing policy data across disconnected spreadsheets and decade-old mainframes isn’t just operational — it’s showing up directly in loss ratios, retention rates, and regulatory exposure.

Insurance software development has moved well past digitizing paper forms. The conversation now is about continuous risk assessment, AI-assisted claims adjudication, composable architectures, and ESG compliance modules. This guide covers all of it — the fundamentals, the 2026-specific shifts, where projects go wrong, and how to decide whether to build or buy.

What Is Insurance Software Development?

Insurance software development is the practice of designing, building, and deploying technology platforms purpose-built for the operational and regulatory realities of the insurance industry. It covers every system that touches the insurance lifecycle — quoting, underwriting, policy issuance, premium billing, claims management, reinsurance accounting, and regulatory reporting.

The critical distinction from general enterprise software development is domain specificity. A rating engine isn’t just a pricing calculator — it has to account for state-by-state rate filings, actuarial tables, risk variables specific to a line of business, and real-time data feeds from external sources. A claims system isn’t a ticketing tool — it orchestrates risk-data pipelines, reserve calculations, fraud scoring, and settlement workflows that carry direct financial and legal consequences.

Custom insurance software development addresses what off-the-shelf platforms can’t: the specific product logic, distribution model, and compliance posture of a particular carrier, MGA, or insurtech. That specificity is both its value and its complexity.

How Insurance Software Development Works

Building insurance software isn’t linear, and teams that treat it like a conventional IT project tend to learn that lesson expensively. The process has distinct phases, each with failure modes specific to the insurance context.

Phase 1: Discovery and Workflow Archaeology

Before architecture decisions or technology choices, the most valuable work is understanding how the business actually operates — not how the org chart says it does. This means embedding with underwriters, claims adjusters, compliance officers, and the operations staff who have built workarounds into their daily routine.

Those workarounds matter. A Florida-based P&C insurer dealing with rapid climate-risk re-ratings, for example, might have underwriters manually overriding system-generated rates using a shared spreadsheet that lives outside the policy admin system entirely. That workaround represents a requirement the system never surfaced — and it’s the kind of thing that only appears when you talk to the people doing the actual work.

Discovery also maps integration dependencies: which external data sources (ISO, LexisNexis, telematics providers, satellite imagery APIs) the new system needs to connect with, and what existing platforms it must coexist with during any transition period.

Phase 2: Architecture — Traditional PAS vs. Composable Insurance Architecture

The most consequential decision in any insurance software project is how the system is structured. For years, the dominant model was the monolithic Policy Administration System — a single platform managing everything from quoting to document generation. That model still works, but its limitations are increasingly apparent when carriers need to launch a new product line, integrate a third-party AI tool, or update rating logic without touching the entire system.

| Dimension | Traditional PAS | Composable Insurance Architecture |

| Structure | Single, tightly coupled platform | Modular, independently deployable services |

| Deployment | Major release cycles (quarterly/annual) | Continuous deployment by component |

| Integration | Vendor-managed connectors | API-first, third-party integration by design |

| Customization | Configuration within vendor constraints | Full control over business logic |

| Risk | Stable but inflexible | Higher initial complexity, greater long-term agility |

| Best For | Standard lines, stable operations | Insurtechs, specialty lines, rapid product launches |

Composable architecture isn’t automatically better — it’s more complex to build and requires stronger internal engineering discipline to maintain. But for carriers that need to update their rating engine without scheduling a six-month vendor release, or integrate a new telematics provider mid-year, the modular approach is increasingly the only viable path.

Phase 3: Development, Compliance Integration, and Testing

Insurance software development follows agile methodologies in most modern engagements, but one consistent failure point is treating the compliance team as a downstream reviewer rather than an embedded participant. Agile works in insurance when the compliance officer is in the daily stand-ups. When they’re handed a completed system for review six months in, the result is usually a significant rebuild.

Testing is more intensive than in general enterprise software. Rating accuracy requires regression testing against historical data. Claims calculations need validation against known outcomes. End-to-end workflow testing has to account for state-specific business rules that may differ across dozens of jurisdictions.

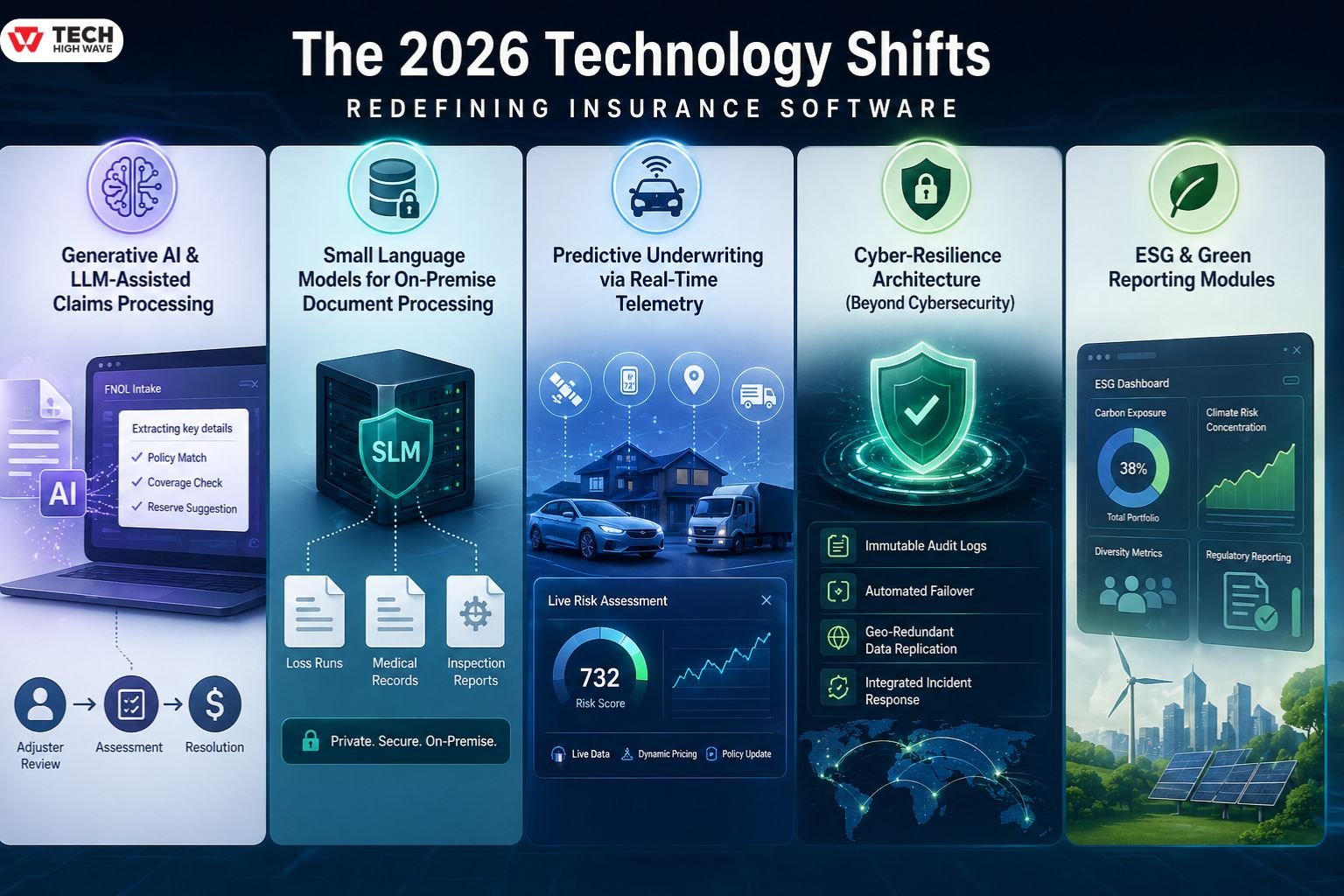

The 2026 Technology Shifts Redefining Insurance Software

The foundational work described above hasn’t changed much. What has changed — significantly — is what “modern” now means at the capability level.

Generative AI and LLM-Assisted Claims Processing

The most operationally impactful AI application in insurance right now isn’t chatbots — it’s using large language models to accelerate FNOL (First Notice of Loss) intake and initial claims adjudication. Systems are now being built to extract structured data from unstructured claim narratives, cross-reference policy terms automatically, flag coverage questions for human review, and generate initial reserve recommendations.

This doesn’t eliminate adjusters. It eliminates the 40% of adjuster time currently spent on data entry and document retrieval, redirecting it toward the judgment-intensive work that actually requires human expertise. Carriers implementing LLM-assisted FNOL workflows are reporting meaningful reductions in average handle time — though realistic timelines for ROI are measured in quarters, not weeks.

Small Language Models for On-Premise Document Processing

Data privacy is a genuine constraint in insurance AI adoption. Many carriers — particularly those handling health-adjacent data or operating under strict state data residency rules — can’t route sensitive policyholder documents through cloud-based LLM APIs. The emerging solution is deploying Small Language Models (SLMs) on-premise: compact, domain-fine-tuned models capable of document classification, extraction, and summarization without sending data outside the organization’s infrastructure.

SLMs trade raw capability for control. They’re not going to generate nuanced coverage opinions, but they’re very effective at extracting structured fields from loss run documents, medical records, and third-party inspection reports — tasks that currently consume significant manual processing time.

Predictive Underwriting via Real-Time Telemetry

Static underwriting — asking applicants a set of questions and pricing based on their answers — is giving way to continuous risk assessment in several lines of business. In auto insurance, telematics has been mainstream for years. What’s different in 2026 is the expansion of this model into property (satellite imagery, IoT sensor data from smart home devices), commercial (GPS fleet data, equipment sensor feeds), and even some specialty lines.

The software implication is significant. A platform designed for static underwriting at point-of-sale doesn’t have the data ingestion architecture, real-time pricing logic, or policy endorsement workflows to support continuous risk assessment. Insurers entering this space need to build (or buy) platforms designed from the ground up for live data feeds — not retrofitted from a questionnaire-based model.

Cyber-Resilience Architecture (Beyond Cybersecurity)

Regulators across the US and EU have moved from requiring cybersecurity policies to requiring demonstrable cyber-resilience — meaning insurers must show not just that they prevent breaches, but that their systems can detect, contain, and recover from incidents without catastrophic data loss or operational failure. For insurance software development, this translates into specific architectural requirements: immutable audit logs, automated failover, data replication with geographic separation, and incident response workflows built into the platform itself.

This isn’t optional in 2026. Several US state insurance departments have adopted NAIC’s cybersecurity model law, and the EU’s DORA (Digital Operational Resilience Act) applies to financial entities, including insurers operating in Europe.

ESG and Green Reporting Modules

ESG disclosure is moving from voluntary to mandatory for insurers operating in EU and increasingly in North American markets. This means insurance software now needs to capture, aggregate, and report ESG-relevant data — carbon exposure in underwriting portfolios, climate risk concentration, diversity metrics in workforce data — in formats aligned with emerging regulatory frameworks.

Building this capability into a policy admin or reporting system after the fact is significantly more expensive than planning for it during initial development. For carriers building or rebuilding platforms in 2026, ESG data architecture is a first-class requirement, not a future enhancement.

2026 Project Health Check: 5 Red Flags to Watch For

Before signing a contract or approving a sprint, evaluate your project against these “Red

Flags.” If more than two are present, your ROI is at risk.

ore launch.

| Red Flag | The Symptom | The 2026 Standard |

| The “Wall of Compliance” | Compliance/Legal are scheduled for a “Final Review” 4 weeks bef | Embedded Compliance: Compliance officers should have “Viewer” access to Jira/DevOps and sign off on User Stories, not just finished code. |

| Data “Lift and Shift” | The vendor says data migration is a “straightforward mapping exercise” using your existing SQL dumps. | Cleanse-First Migration: 2026 systems require high-integrity data for AI modules. You must budget for a separate data cleansing phase <em>before ingestion. |

| Black-Box Logic | The rating or claims engine provides an “output” but can’t show the step-by-step logic path for a specific state’s regulation. | Explainable Architecture (XAI): Every automated decision must have a “logic log” to satisfy state auditors and prevent litigation. |

| The “ACORD” Void | Your development team asks, “What is an ACORD 125?” during the discovery phase. | Domain-Native Teams: Your architects must speak the language of ISO, NCCI, and ACORD fluently to avoid reinventing the wheel. |

| The “Big Bang” Release | The roadmap shows a single “Go-Live” date 18 months away with no interim functional releases. | Phased Delivery: You should be able to push a single “Micro-module” (like a new FNOL intake) to production within 4 months. |

Build vs. Buy: A Decision Matrix

One of the most consequential and frequently rushed decisions in insurance technology is whether to build custom software, buy a commercial platform, or pursue a hybrid approach. There’s no universally correct answer — but there is a framework.

| Factor | Lean Toward Building | Lean Toward Buying |

| Lines of Business | Specialty, non-standard, or highly differentiated products | Standard personal lines or commercial lines |

| Organization Size | Large carrier or well-funded insurtech | Small-to-mid carrier with limited IT capacity |

| Speed to Market | Longer runway acceptable; differentiation is the priority | Need to launch within 6–12 months |

| Integration Complexity | Unique data sources or proprietary workflows | Standard third-party integrations (ISO, LexisNexis) |

| Regulatory Environment | Multi-state with highly specific compliance logic | Single-state or limited jurisdiction |

| Internal Engineering | Strong in-house or embedded development team | No dedicated software development function |

The hybrid model — buying a commercial PAS for core functions and building custom modules for differentiated capabilities — is increasingly the pragmatic middle ground. It reduces time-to-market while preserving flexibility where the business actually competes on product or process.

Why Insurance Software Directly Affects Loss Ratios

This is the conversation that tends to get CFOs and CEOs engaged when technology projects otherwise struggle for executive attention: custom-built insurance software isn’t a cost center. When implemented correctly, it’s a margin protector.

The mechanisms are specific. Automated underwriting rules reduce the rate of adverse selection by applying consistent eligibility criteria at scale. Real-time fraud scoring on inbound claims reduces leakage before reserves are set. Straight-through processing for low-complexity claims reduces handling costs. Configurable rating logic enables faster response to emerging loss trends — which matters enormously when climate or litigation patterns are shifting a book’s underlying loss profile.

A carrier that can re-rate a property portfolio in response to updated wildfire exposure models within days rather than months isn’t just technically superior — it’s operationally positioned to maintain combined ratios that a slower competitor cannot match.

Common Mistakes That Derail Insurance Software Projects

Even well-resourced projects run into avoidable failures. These patterns repeat consistently across the industry.

<strong>Underestimating data migration. Moving decades of policy and claims history from a legacy system to a new platform is almost always harder than scoped. Historical data is inconsistent, structures don’t translate cleanly, and edge cases discovered mid-migration can require significant replanning. Budget for it accordingly.

Excluding compliance from development. Compliance teams handed a completed system for review reliably identify issues that require substantial rework. The more effective model is embedding compliance review into sprint cycles — reviewing features as they’re built rather than after the system is complete.

Overbuilding the initial scope. The instinct to specify the complete platform on day one is understandable and consistently expensive. Phased delivery — starting with the highest-pain workflows and building from there — reduces risk, accelerates value realization, and ensures real user feedback shapes subsequent development.

Ignoring domain expertise on the vendor side. General software engineering talent can build almost anything. But teams without insurance-specific knowledge will reinvent standard solutions — and miss non-obvious requirements — at the client’s expense. ACORD familiarity, line-of-business experience, and regulatory knowledge matter as much as technical capability.

Conclusion

Insurance software development in 2026 is a fundamentally different challenge than it was five years ago. The foundational work — discovery, architecture, compliance integration, testing — remains demanding. But layered on top is a set of emerging capabilities — AI-assisted claims processing, continuous risk assessment, cyber-resilience frameworks, ESG reporting — that are moving from differentiators to table stakes faster than most organizations anticipated.

The carriers and insurtechs that treat technology investment as a strategic lever — not a maintenance cost — are the ones compressing loss ratios, accelerating product launches, and building distribution relationships that competitors struggle to replicate. Custom insurance software development, done with the right domain expertise and architectural discipline, is one of the clearest paths to that outcome.

Frequently Asked Questions

Q1: What is insurance software development?

Insurance software development is the process of building digital platforms that manage the full insurance lifecycle.

Q2: How is insurance software development different in 2026?

Modern insurance software development increasingly incorporates generative AI for claims processing, real-time telemetry for continuous underwriting, composable architecture for faster product launches, and mandatory ESG reporting modules — capabilities that didn’t exist at scale in previous years.

Q3: How long does custom insurance software development take?

A focused module such as a claims intake portal typically takes three to six months.

Q4: What is the difference between a traditional PAS and composable insurance architecture?

A traditional Policy Administration System is a single, tightly coupled platform. Composable insurance architecture uses independent, API-connected modules.

Q5: How much does insurance software development cost?

Costs vary widely by scope. Focused platforms typically range from $150,000 to $500,000. Enterprise core system replacements commonly exceed $1 million.

Q6: What compliance requirements apply to insurance software in 2026?

Relevant frameworks include NAIC cybersecurity model law provisions, DORA for EU-operating insurers, HIPAA for health-adjacent data, SOC 2 for data security, and ACORD standards for interoperability. ESG disclosure requirements are also becoming mandatory in several jurisdictions.

For More Visit: TechHighWave