Money problems rarely come from a lack of income. They come from blind spots — like forgetting that $15 streaming subscription you signed up for three months ago, or overspending on small daily purchases that quietly add up. I’ve seen it firsthand: people earn well, yet by the end of the month, their “leftover” money mysteriously disappears.

That’s why searches for top free personal finance software keep rising. People aren’t looking for motivation or generic tips — they want clarity, control, and systems that actually work in real life.

Most “best free finance software” articles are stuck in the Mint era: repeating the same tools, glossing over limitations, and pretending “free” still means unlimited automation. This guide is different.

Here, you’ll find the best free personal finance software to unlock your financial potential in 2026, practical warnings about limitations, and a $0 hybrid stack that gives clarity without costing a dime. No hype, no promises of overnight financial freedom — just tools and systems that help you make better financial decisions and maintain control.

What “Free Personal Finance Software” Really Means in 2026

In 2026, “free” rarely means unlimited. Most free personal finance apps now offer:

-

Core functionality at no cost

-

Manual entry instead of full automation

-

Limits on bank or brokerage connections

-

Optional (and sometimes aggressive) upsells

This isn’t necessarily bad. Many people manage money better with simpler tools and fewer automations. The goal isn’t perfection — it’s finding a tool you can realistically use consistently.

⚠️ 2026 Warning: Bank Sync Is Expensive and Limited

Automatic bank syncing is no longer guaranteed on free apps. Services like Plaid and Yodlee charge platforms per connection, which means many free apps now restrict the number of linked accounts or limit refresh frequency.

What this means for you:

-

Free plans may allow only 2–3 linked accounts

-

Data refreshes may be delayed by hours or even days

-

Manual entry is often the default, especially for smaller accounts

Manual tracking may actually be a feature, not a flaw, because typing “$12 for coffee” yourself builds awareness far better than automatic imports. If a free app promises unlimited syncing forever, be skeptical — it’s likely unsustainable for the provider.

Tip for efficiency: Use apps that allow quick CSV imports or bulk editing to save time while still maintaining awareness.

The Best Free Personal Finance Software (2026)

Categories at a Glance

| Category | Tools |

|---|---|

| Budgeting | HomeBank, EveryDollar, YNAB (Trial) |

| Full Control & Privacy | GnuCash, Money Manager Ex |

| Net Worth Tracking | Personal Capital (Empower), Wealthica |

| Investing & Markets | Sharesight, Yahoo Finance |

| Simplicity | PocketGuard |

1. GnuCash — Full Control and Privacy

Best for: Advanced users, privacy-conscious individuals

GnuCash is open-source, desktop-based, and uses double-entry accounting — the same system professionals rely on.

Why it stands out:

-

Full control of financial accounts

-

Works offline; your data is never uploaded

-

Detailed reports for cash flow, net worth, and investments

Real-world tip: If you want a permanent financial archive, export GnuCash data monthly. Even if the software updates or disappears, you’ll maintain a complete record.

Limitations:

-

Steep learning curve

-

An outdated interface can feel clunky

-

Not mobile-first

Example:

Alex, a freelance graphic designer, uses GnuCash to track every client invoice and tax-deductible expense. He prefers manual entry because it forces him to notice anomalies immediately — something automated tools often hide.

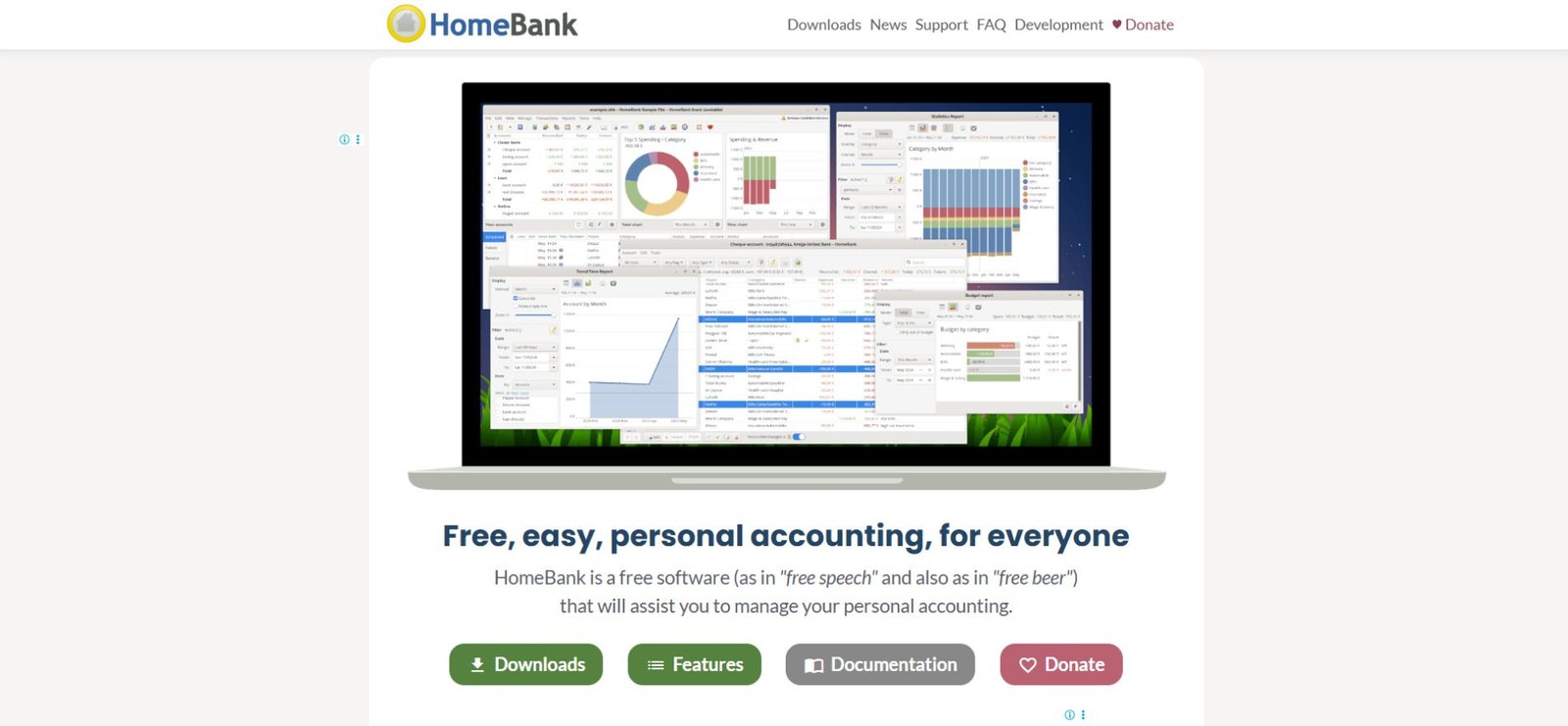

2. HomeBank — Simple Household Budgeting

Best for: Beginners and households

HomeBank focuses on clarity. It shows exactly where money comes from, where it goes, and what’s left.

Strengths:

-

Clean dashboards

-

Simple income vs. expense tracking

-

Household budgeting features for couples or families

Limitations:

-

No live bank syncing

-

Manual imports required

Example:

Sara and Mike, a young couple, use HomeBank to track household bills. They manually log expenses every Sunday, which doubles as a short weekly review. This habit prevents overspending on recurring subscriptions.

3. Personal Capital (Empower) — Free Net Worth Tracker

Best for: Big-picture financial visibility

Why it works:

-

Real-time net worth updates

-

Investment fee analysis and retirement projections

-

Long-term goal tracking

Trade-offs:

-

Limited budgeting tools

-

Advisory upsells for users with assets over ~$100,000

Tip: Use Personal Capital as your big-picture dashboard — combine it with a budgeting app for daily control.

Example:

Jane tracks her three brokerage accounts and checking account through Personal Capital while using EveryDollar for day-to-day expenses. The combination keeps her aware without overwhelming her.

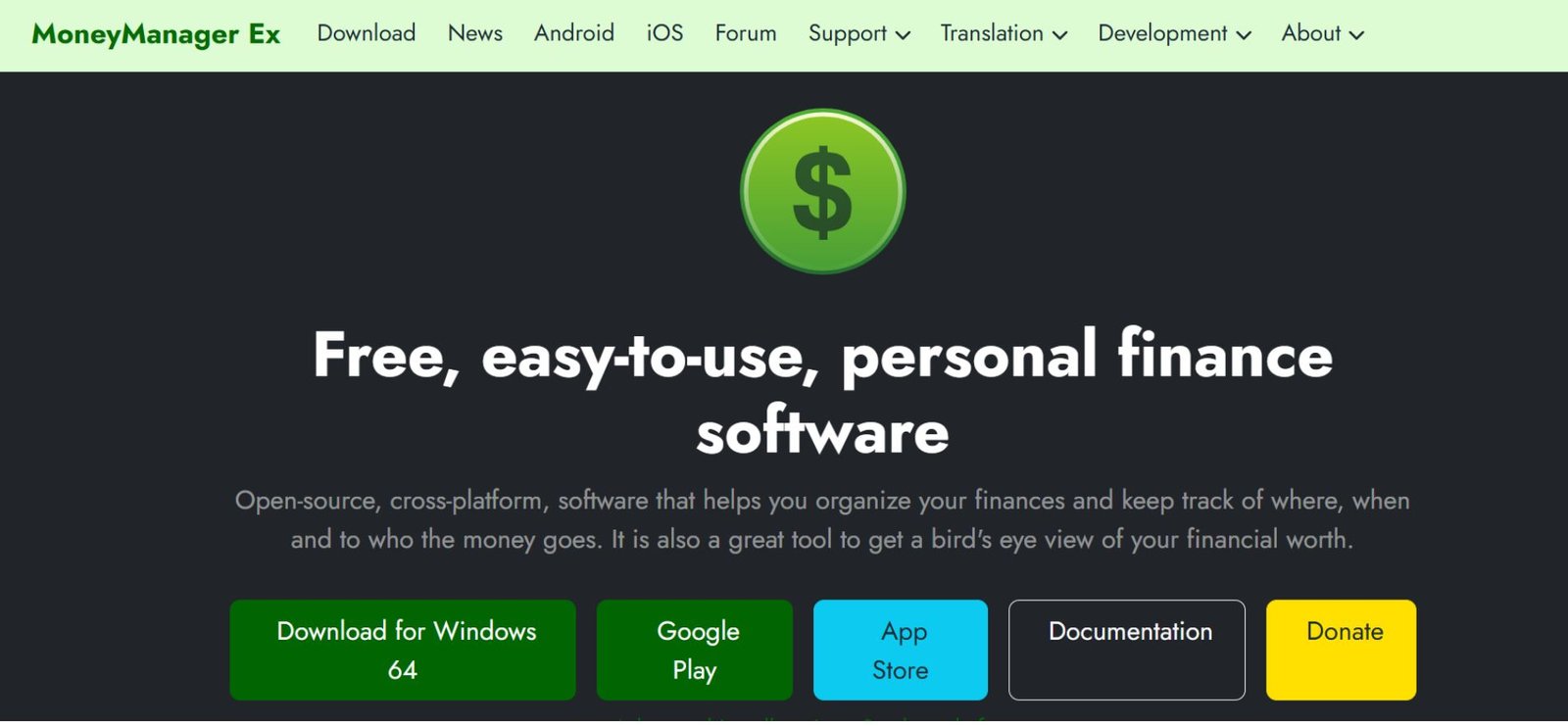

4. Money Manager Ex — Lightweight Desktop Tool

Best for: Quick, offline money tracking

Highlights:

-

Lightweight and fast

-

Offline use ensures data privacy

-

Simple financial reporting

Limitations:

-

Basic visuals

-

Limited automation

Example:

Liam, a privacy-focused software engineer, uses Money Manager Ex to track side-hustle income. The offline feature reassures him that no third party can access his data.

Also Read: How Does Zelle Make Money? The Real Business Model Explained (2026)

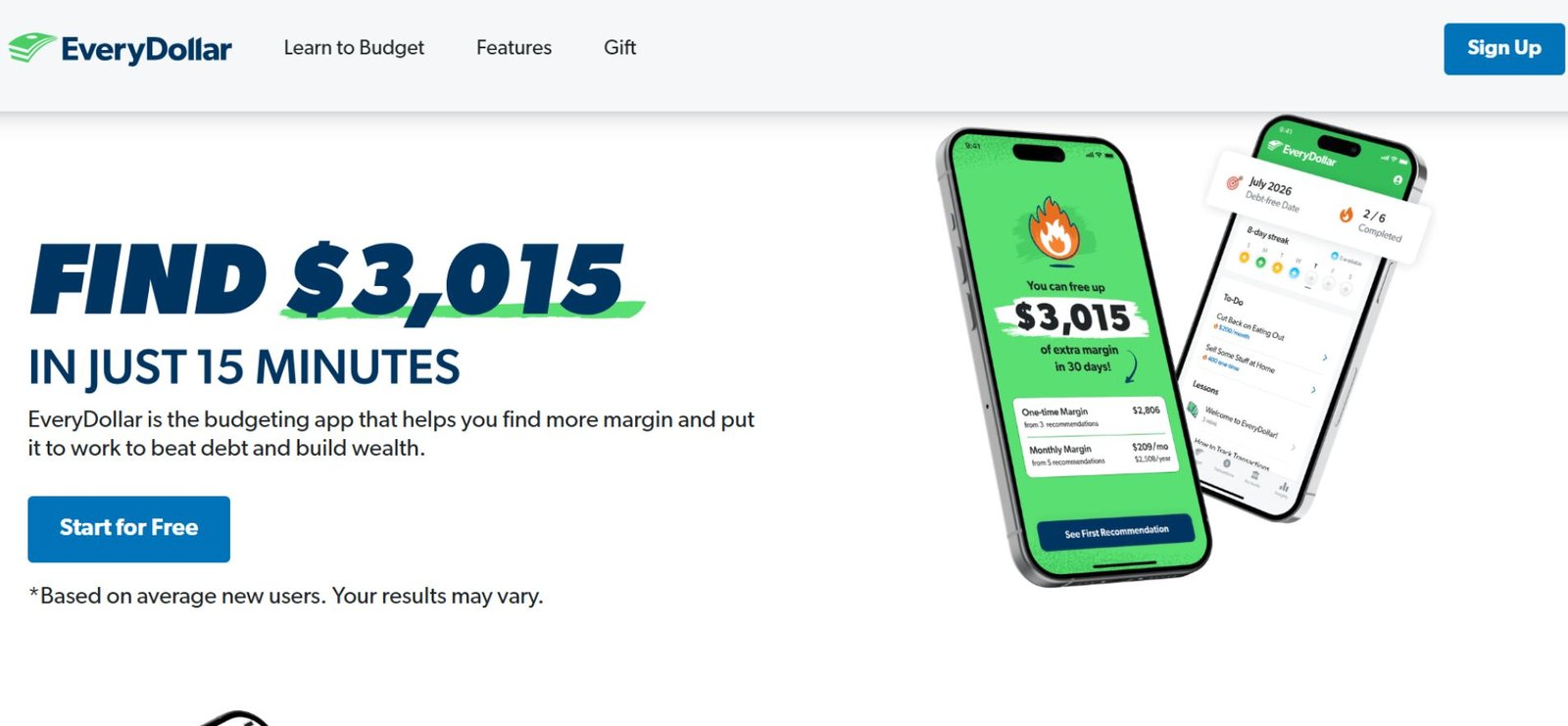

5. EveryDollar (Free Version) — Zero-Based Budgeting

Best for: Spending discipline

Why it works:

-

Manual entry encourages awareness

-

Clear monthly planning

-

Simple, intuitive category structure

Limitations:

-

Manual transactions only

-

Upsells for premium features

Tip: The manual aspect isn’t a flaw — typing your expenses builds awareness and can change behavior more effectively than automatic tracking.

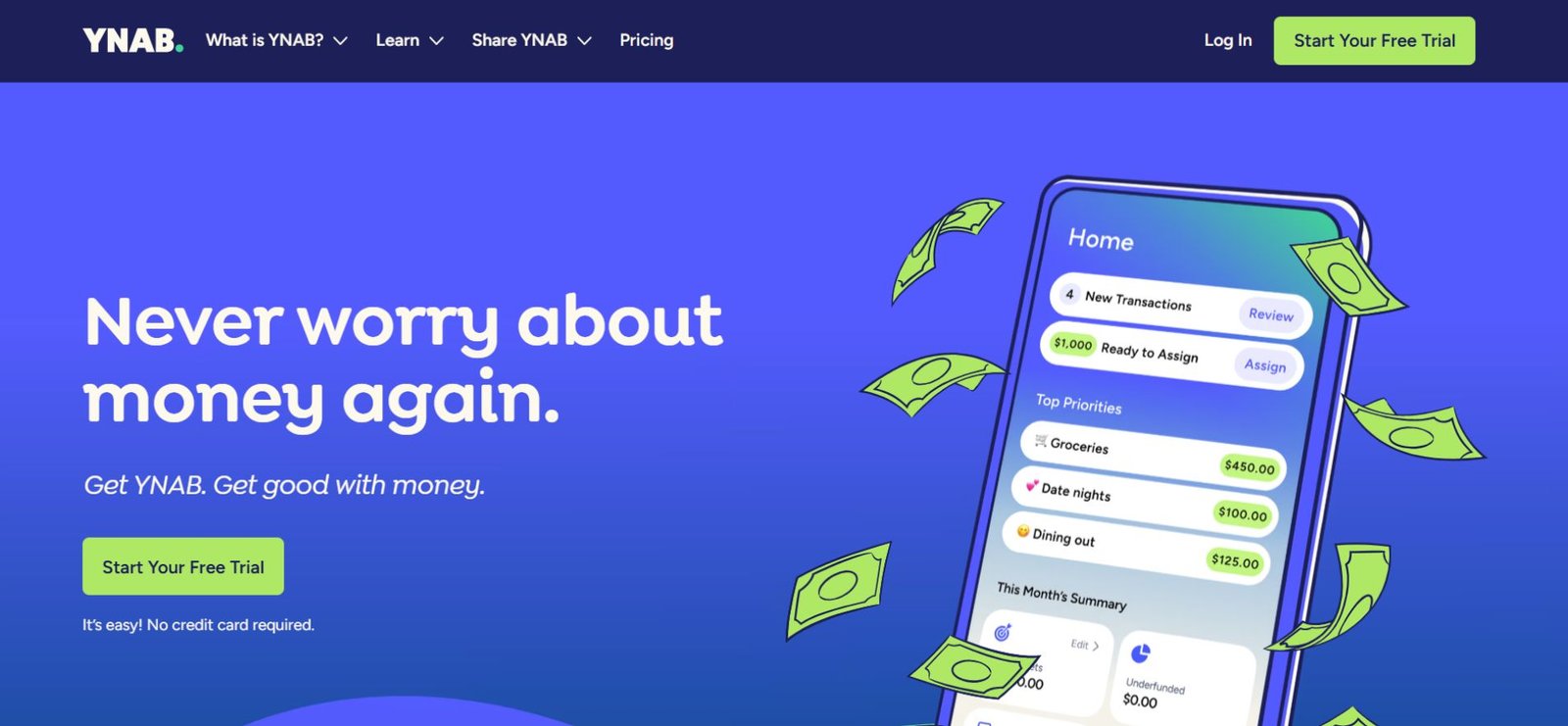

6. YNAB (Free Trial) — Behavioral Budgeting

Best for: People who overspend despite decent income

Why it works:

-

Envelope budgeting system

-

Focus on future expenses, not just past spending

-

Educational resources and tutorials

Limitations:

-

Paid subscription after trial

-

Requires habit formation

Example:

Chris, a recent grad, used YNAB’s 34-day free trial. He formed the habit of planning every dollar before spending. Even after switching to EveryDollar, the behavioral patterns stuck.

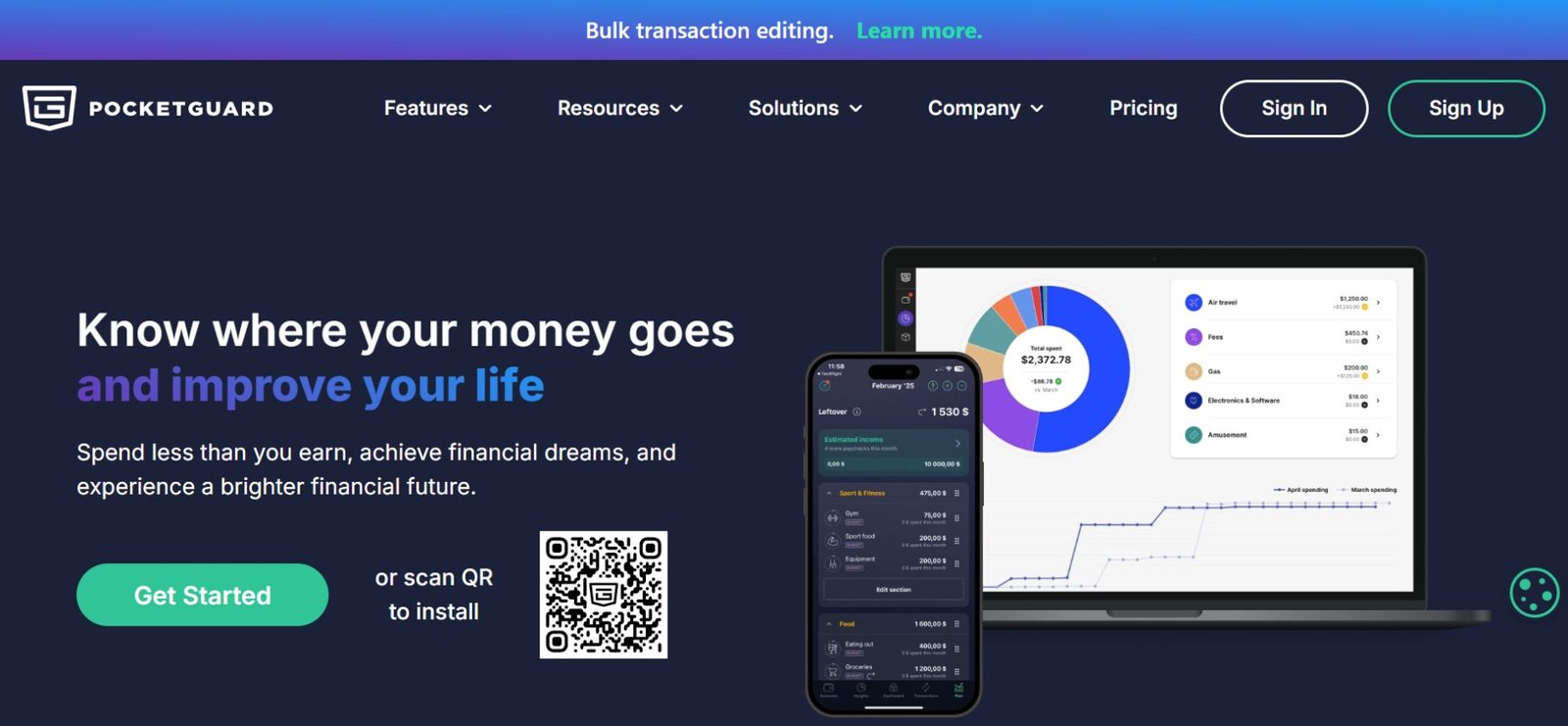

7. PocketGuard — Quick Spending Awareness

Best for: Mobile-first users

Why it works:

-

Shows “safe-to-spend” money

-

Simple, clean mobile interface

-

Quick daily insights

Limitations:

-

Reduced free features compared to premium

-

Less category control

Tip: Best used as a daily check-in to prevent small, unintentional overspending.

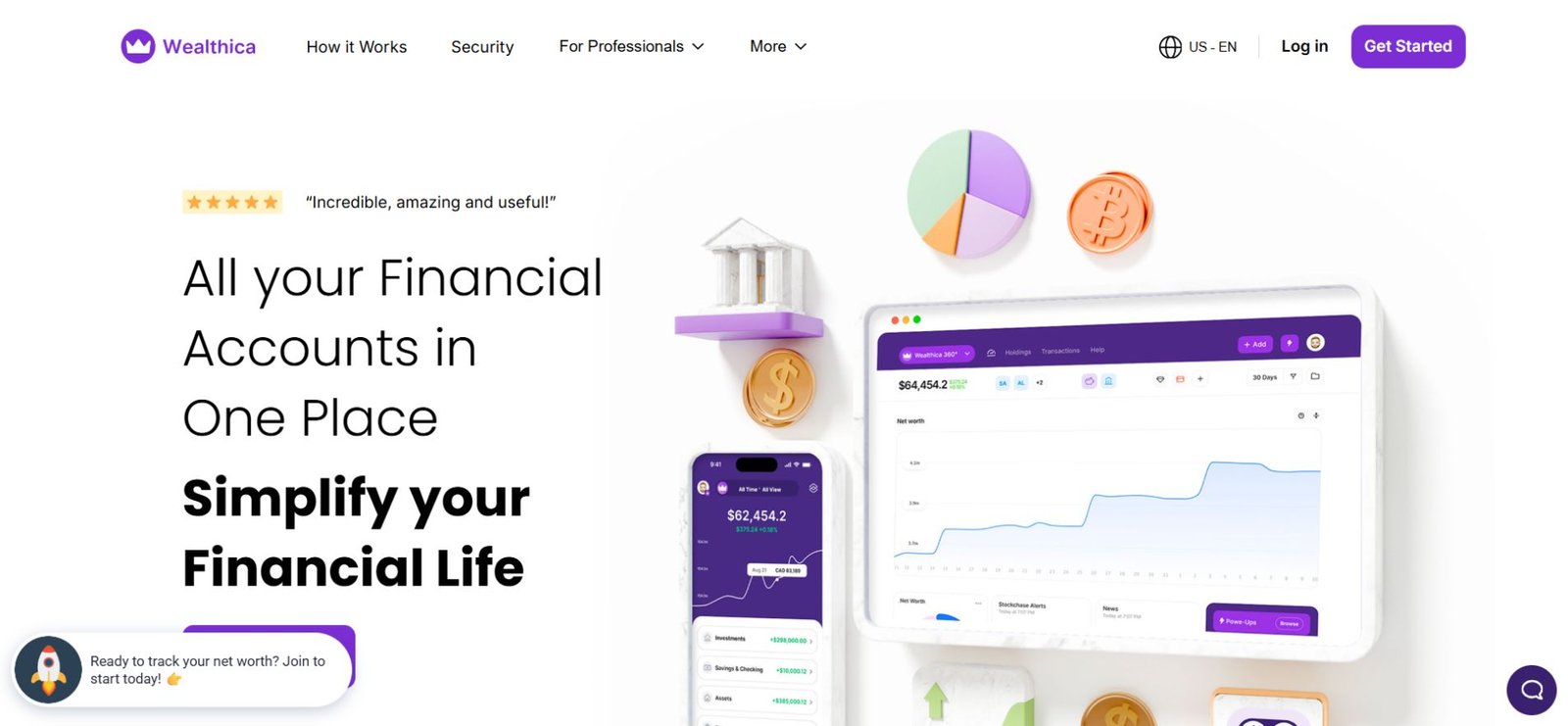

8. Wealthica — Investment Aggregation

Best for: Tracking multiple investment accounts

Highlights:

-

Consolidates portfolios in one dashboard

-

Clean visuals for allocation and performance

-

Useful for long-term monitoring

Limitations:

-

Free tier limits linked institutions to 2–3 accounts

Example:

Freelancer Maria tracks her RRSP, TFSA, and brokerage account on Wealthica. She exports data quarterly to maintain an offline copy, ensuring continuity even if the app changes terms.

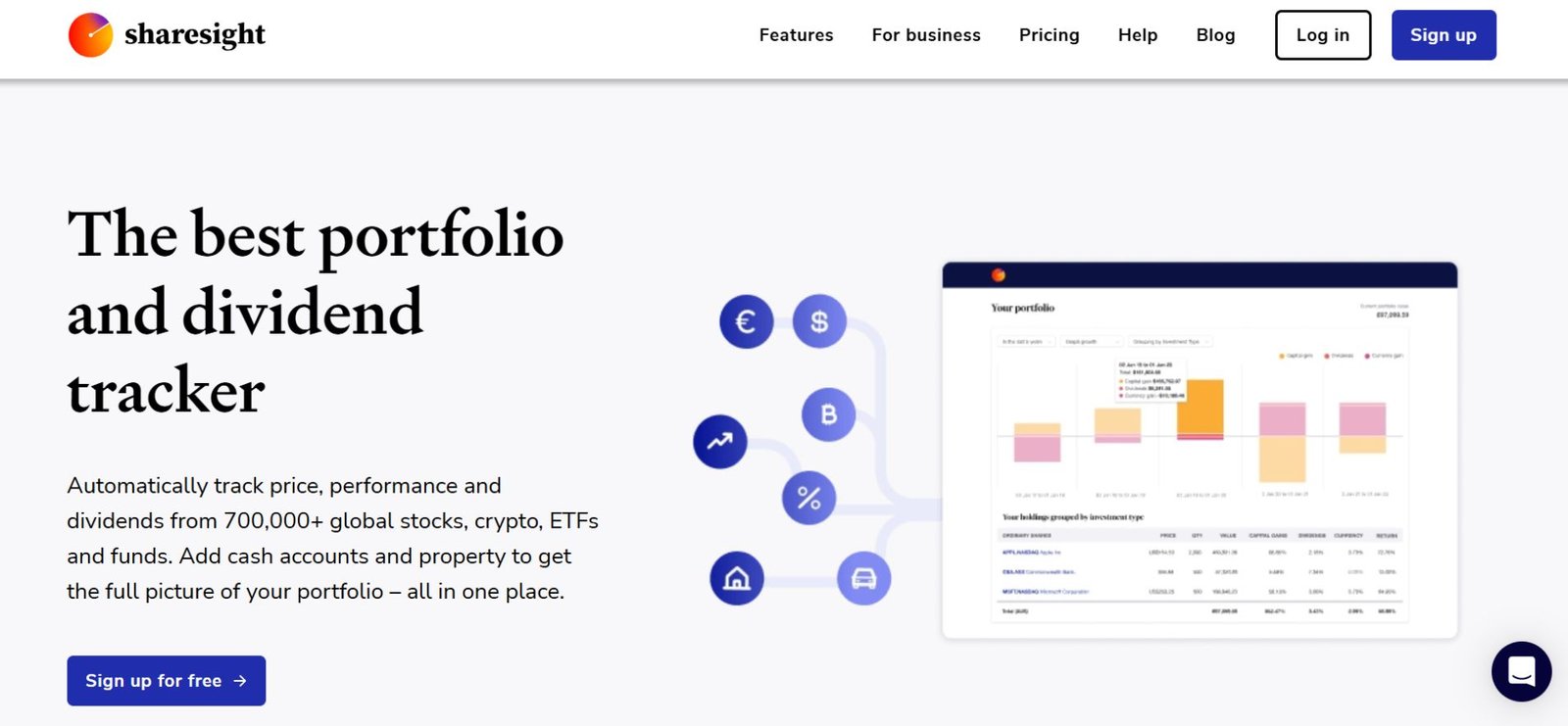

9. Sharesight — Free Investment Performance Tracker

Best for: DIY investors

Why it works:

-

Tracks dividends and capital gains

-

Performance analytics

-

Tax-friendly reports

Limitations:

-

The free plan allows up to 10 holdings, which may be limiting for diversified portfolios

Tip: Use Sharesight for focused portfolio tracking. For additional holdings, supplement with Yahoo Finance watchlists.

10. Yahoo Finance — Market & Portfolio Tool

Best for: Monitoring investments and watchlists

Why it works:

-

Real-time market data

-

Unlimited watchlists

-

Broad asset coverage

Limitations:

-

Not a budgeting tool

-

Limited cash-flow features

Tip: Combine Yahoo Finance with a budgeting app to monitor investments and cash flow simultaneously.

How to Choose the Right Tool

-

Identify your goal: Daily spending control, long-term insight, or both

-

Decide your priority: Privacy, automation, or ease of use

-

Match tools to your workflow: Budgeting vs net worth vs investing

Tip: One app rarely does everything well. Combining tools often yields better control.

Also Read: Best Family Tree Software: Organize Your Genealogy Easily

The $0 Hybrid Stack — How Savvy Users Do It in 2026

| Task | Recommended Tool | Why |

|---|---|---|

| Daily spending | EveryDollar (Free) | Manual entry builds awareness |

| Net worth | Personal Capital | Best free big-picture dashboard |

| Long-term archive | HomeBank | Offline permanent record |

| Investments | Yahoo Finance | Unlimited watchlists, no holding limits |

Example:

Jane, a recent grad with 3 bank accounts and 2 investment apps, manually enters daily expenses in EveryDollar and checks net worth monthly in Personal Capital. Cost? $0. Stress? Minimal.

Tip: Review your stack quarterly and adjust tools as your financial needs evolve.

Common Mistakes

-

Chasing features instead of building habits

-

Using too many apps without a system

-

Ignoring monthly reviews

-

Expecting software to automatically solve behavior

Reality: Most people abandon tools not because they’re bad, but because they forget to check them consistently.

2026 Trends in Personal Finance Software

-

Fewer fully free tools

-

Rising privacy regulations

-

AI-assisted categorization (still unreliable, especially for irregular income)

-

Hybrid systems outperform all-in-one apps

Simplicity is winning — mostly because people are tired of bloated apps and constant notifications.

Real-World Rules That Matter

-

Manual entry builds awareness — a feature, not a flaw

-

Always check CSV export — ownership of data is critical

-

Be cautious with free AI financial advice — often just ads or upsells

FAQs

Q1. What is the best free personal finance software in 2026?

For most users, HomeBank is ideal for budgeting, while Personal Capital (Empower) is the top choice for tracking net worth and investments. Combining both gives a comprehensive $0 financial system.

Q2. Is free personal finance software enough for long-term planning?

Yes — free software can support long-term financial planning, as long as you review accounts consistently and maintain realistic goals. Manual tracking often improves awareness over fully automated apps.

Q3. Are free personal finance apps safe to use?

Open-source tools like GnuCash or reputable platforms like Personal Capital are generally safe when used responsibly. Avoid apps with unclear privacy policies or excessive third-party sharing.

Q4. Do I need more than one personal finance tool?

Often, yes. Many free apps focus on either budgeting, net worth, or investment tracking. Using a hybrid stack allows full visibility without paying for premium features.

Q5. Which free personal finance software offers the best privacy?

For maximum data control, desktop apps like GnuCash and Money Manager Ex keep your financial information offline, preventing third-party access.

Q6. Can I build a full personal finance system for $0?

Absolutely. A hybrid system combining:

-

EveryDollar or HomeBank for budgeting

-

Personal Capital for net worth

-

Yahoo Finance or Sharesight for investments

…provides full financial insight without any subscription fees.

Q7. What free app is best if I only want to track spending?

EveryDollar and PocketGuard are excellent for daily expense tracking, offering simple interfaces and reminders without overwhelming features.

Q8. What is the easiest way to combine free apps effectively?

Use a hybrid stack approach:

-

Daily spending → EveryDollar

-

Net worth → Personal Capital

-

Investment tracking → Yahoo Finance or Sharesight

This system ensures complete visibility while remaining cost-free and manageable.

Final Thoughts

The best free personal finance software isn’t the one with the most features. It’s the one you’ll actually use consistently.

Pick a simple system. Review monthly. Adjust quarterly. That’s how real progress happens.

Related: BE1 Crypto Explained: What It Is, How It Works & Is It Legit (2026)